There has been a lot of talk about Edmonton’s debt recently, with some candidates going so far as to highlight debt as a key election issue. Debt is one of those topics that is easy to complain about but difficult to understand. Throwing out a billion-dollar number and proclaiming it bad is easy, understanding how we got to that number in the first place and how it fits into the broader context of the City’s financial situation takes more effort.

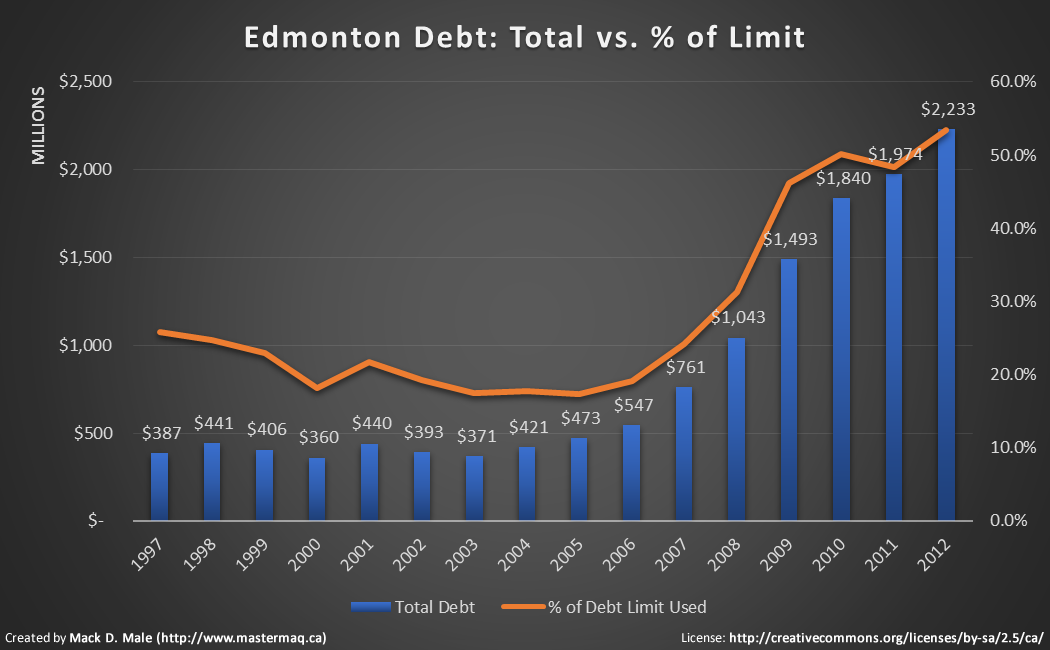

Here’s a look at Edmonton’s debt history for the last fifteen years:

So we can see that at the end of 2012 our city’s debt totaled $2.2 billion, which is 53.4% of our debt limit as outlined by provincial legislation. Is that high or low? Let’s make some comparisons. Here’s what Edmonton’s per capita debt looks like compared with Calgary:

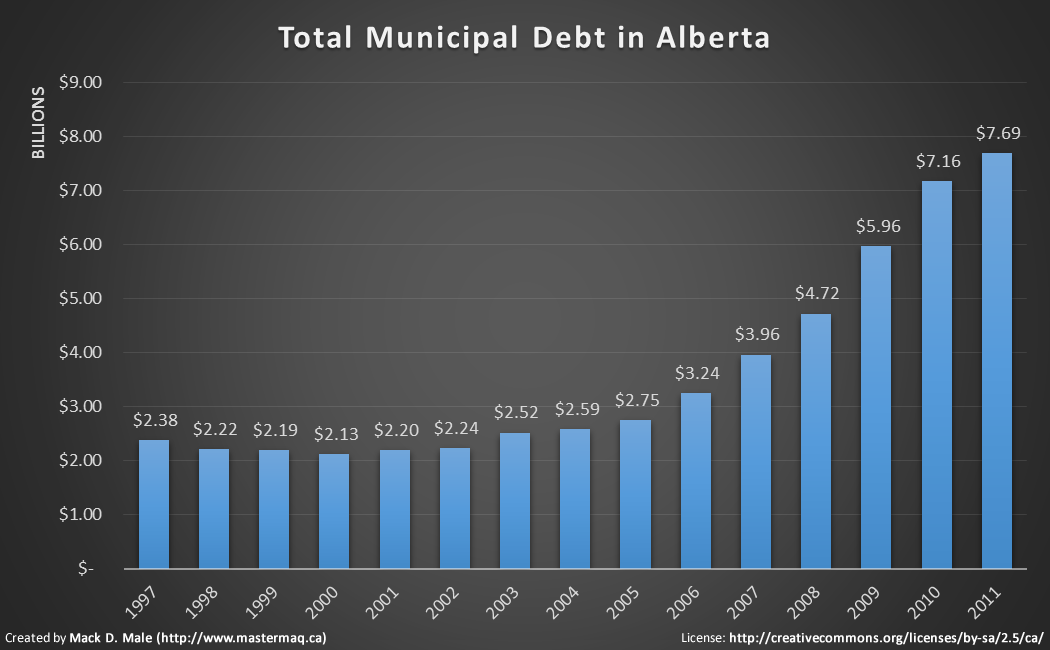

So we’ve got less debt per person than Calgary does, and have had significantly less over the last decade. What about the rest of the province? Municipalities collectively owed about $7.7 billion at the end of 2011, with Calgary and Edmonton together accounting for 69% of that amount.

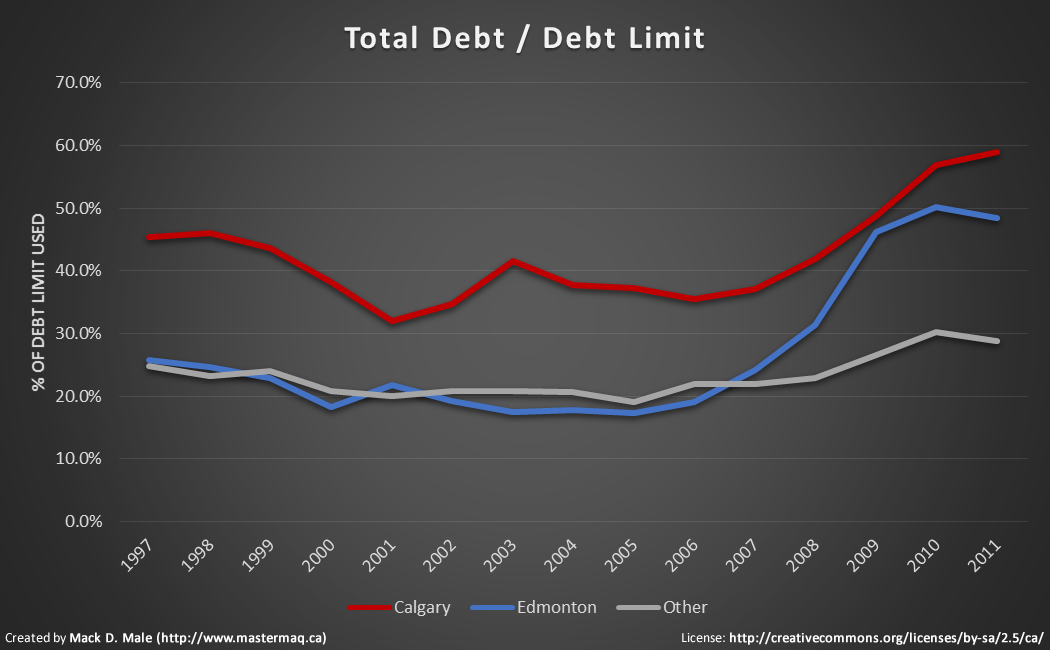

Here’s a comparison of the amount of available debt used by Calgary, Edmonton, and all other municipalities grouped together:

Notably Edmonton has used less of its available debt than Calgary, with the gap narrowing only in the last few years. It wasn’t until 2003 that we started to take on more debt. Why is that? And what is the impact?

Here’s what current Ward 6 candidate Scott McKeen wrote in the Edmonton Journal back in 2003:

And of all the cities in Canada, Edmonton stands out for being a skinflint among cheapskates. Our per capita debt is about one-fifth of Calgary’s and one-tenth of Vancouver’s.

As you’re maybe already aware, Edmonton’s hell-bent determination these past two decades to eliminate civic debt has created its own set of problems: neglected and decaying roads; inferior civic services; dated, second-class public facilities.

But we so loved the idea of getting out of debt that we ignored our mounting repair bills. We also ignored the fact that some other cities — Calgary and Vancouver, for example — were busy borrowing money to pave the way for growth.

The kind of debt Edmonton has taken on in recent years is “smart debt”, money for which the debt servicing costs are tied to revenue. It’s not debt for operating costs, it’s another financing tool the City can use to build the infrastructure we desperately need.

The 2007 Debt Management Fiscal Policy Review also discussed this history:

At the end of the 1970s, tremendous growth pressure resulted in a relaxation of the City’s debt limit, leading to a threefold increase in the City’s annual borrowing. This resulted in Edmonton’s tax-supported debt being higher than most other major Canadian cities at that time.

The recession of the early 1980s and high interest rates necessitated a revised Policy. Under this new debt policy, tax-supported debt issues were limited to $25 million per year. Moreover, new tax-supported borrowing was prohibited after 1990. Subsequent to 1990, an exclusive pay-as-you-go approach was adopted for capital expenditures. Shorter borrowing terms for utility debt (self-liquidating) were also required.

In 2002, to address growing infrastructure issues and flat sources of financing, tax-supported debt was reintroduced through an amended Policy. A five-year borrowing guideline called for an annual approval of $50 million in debt-financed projects for 2003-2007, totalling $250 million. Adoption of the five year guideline has enabled the City to construct a number of much needed projects such as fire halls, a senior’s centre, libraries, parks, an interchange and other road works.

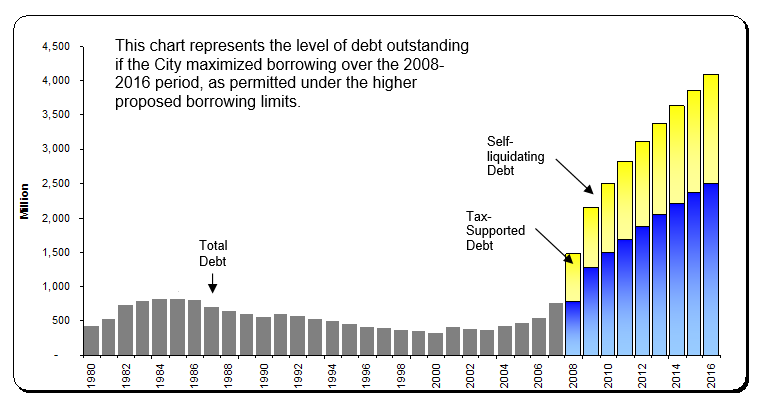

It also included this chart which shows the amount of debt Edmonton had outstanding throughout the 1980s and projected amounts through 2016 as permitted under higher borrowing limits:

The jump might look significant, but Edmonton’s outstanding debt is still well within both the provincial debt limits and the City’s own more strict debt limits. The City’s credit ratings remain very strong.

It’s true that Edmonton’s debt has grown significantly over the last decade. But it’s also true that taking on that debt has enabled us to invest in much-needed infrastructure to support our growing city. Candidates that don’t recognize this risk pursuing a policy that would take us back to the 1990s, reversing any progress we’ve made toward tackling our ever-growing infrastructure deficit. As the City says, “an appropriate and sustainable level of tax-supported debt is recognized as a legitimate part of any long-term capital financing plan.”

Note: Much of the data in this post came from the Government of Alberta. While figures are available for 1994-1996 at that site, I excluded them because the values for Edmonton were highly inconsistent with the rest of the data and were extremely different from the City of Edmonton’s published values for those years. I have submitted an inquiry about the validity of the data.

Really excellent analysis, Mack – thanks very much!

thanks, Mack, for constructing some graphs to clearly illustrate the situation; i had been curious about such things.

just the one impression… for a long time, Edm had a stable (albeit growth-limiting) debt of ~0.4B. as you and others have said, this is not necessarily a good idea, as we cannot replace ageing infrastructure *plus* build the new infrastructure that is needed to support a growing city. so, debt and especially “self-liquidating debt” is a good thing.

But within limits, of course. it perturbs me to see the debt steadily increasing. one would hope/expect to see it level off at a higher but more reasonable number. i don’t think that the debt limit is that meaningful a limit; it seems like an arbitrary line in the sand. ditto for the fact that we still have an excellent credit rating and can borrow at excellent rates; that’s good to know, but…

I’m thinking it would be useful to do some analysis to understand what would be a useful limit, whether it’s a hard limit (say 5B) or a percentage of the debt limit

again, good work!

Thanks for the comment. While our debt has been steadily increasing, we’ve also seen increases throughout the province as a result of changes to the borrowing limits, so it’s not a situation that is unique to Edmonton. We also don’t seem to be at risk of losing large numbers of people, thus we don’t have much risk about a decrease in revenue.

I think looking at debt servicing limits is potentially more interesting than total debt limits. We need to be able to afford the debt servicing costs on an ongoing basis.

Good debt, bad debt…..both are largely irrelevant in the grand scheme of things. The problem is not the amount of debt piling up – it’s HOW we are going to pay it off. Right now, no mayoral candidate has a clue as to how they will increase municipal revenues. Investing in better roads and infrastructure is all fine and dandy except it doesn’t help pay the bills. Maybe if we had toll roads…….but that’s a whole other discussion.

Edmonton already has plans to pay of each bit of debt it has incurred. It’s actually part of the cities bylaws that there must be a plan in place to pay off each piece of debt that is taken on. Next.

Plan? What plan? I don’t care what the city bylaw says. Just because they are legally required to have a plan in place doesn’t necessarily mean it will be an EFFECTIVE one, which was my point to begin with. In fact, find me links which shows this “plan” – I would like to look at it.

Detroit is only notable because its an exception, and anecdote really.

Hardly. It’s just the first in what is going to be a whole bunch in the next few years. Windsor may be one of them.

To call it “anecdotal” is trivializing what is a serious systematic problem.

Citations needed

So our debt is okay because others are in more debt? Because it follows provincial guidelines? This is a perfect example of an entire column that does not address the actual issue. This is exactly what created the mortgage crisis in the United States. Just because we can, does not mean we should; and just beause legislation allows it, does not make it right. The fundamental problem is one of priorities, and ability to pay Cities should not be able to borrow privately, financing should only come through taxes, or bond issues; any other method ultimately leads to the kind of global financial mismanagement that has occurred over the last twenty years or longer! People find money for discretionary consumer spending, but when it comes to essentials; a significant number complain. Governments are no different … politics makes for poor government. The amount of time Edmonton city council has spent on the arena complex far outweighs it’s worth!

if you cannot find 10,000 investors with $10000.00 to finance the project, why should you borrow money? Because it is easier than asking people for money: and governments have been borrowing for a long time. It is time to stop the practice, or put greater limitations on it. Economic survival does not depend on taking on debt, it depends on taking caring of essentials first, and a more equitable distribution of resources. Sharing is one of the hardest things to teach children, but adults are no better; everyone wants to take the easy way out, or what seems to be the easy way; until there is another debt crisis.

How is finding 10,000 investors with $10000.00 different than borrowing money? Unless your idea of investing is a Ponzi scheme, investors need to be repaid too.

There is no difference. But if what you say is valuable, and necessary; but if no one is actually willing to risk their own cash…then it is all media hype, and politics; and not really a priority, or necessary. The Roman Empire had games, and arenas too.

Way to serve up faulty generalizations with a side of red herring. There is a substantial difference between “no one willing to risk their own cash” and “10,000 investors with $10000.00”. Any enterprise that society deems would be unmoral to be run for profit is unlikely to to be run by private financing – is health care all media hype? Public transport? Education?

As for the Romans, they could get away with slaves building an open-air arena.

So, Edmonton taxpayers are 2.3 BILLION Dollars in debt and we don’t have a debt problem? Whoa !. .Who is Mack D Male and who does he support for Mayor?

Walmart, #1 on the Fortune 500 list, has a debt of $57.2 billion. Royal Dutch Shell carries a debt of $32.97 billion.

Berkshire Hathaway? $63.95 billion in debt.

Smart businesses operate on credit. Bad businesses rely only on the cash they’ve stashed under a mattress.

I disagree on your conclusion – and can’t believe you can so blithely make that claim. The real question is what is an appropriate amount of debt? Your preference may not be mine – and indeed it depends on a host of factors like my age, my income prospects, current pressures on services, LT demographic trends etc. These are complex factors. It is not a wish list paid for by whomever is left holding the tab.

Do you need personal loan? Does your firm,company or industry need financial assistance? Do you need finance to start your business? Do you need finance to expand your business? We give out loan to interested inviduals who are seeking loan with good faith. Are you seriously in need of an urgent loan contac us at Email: honestloan10@gmail.com

APPLICATION DETAILS

Your Full Details:

Full Name:

Loan Amount Need:

Loan Duration:

Phone Number:

Applied before?

State:

Monthly Income:

Country:

You are to send this to our Company Email Address: honestloan10@gmail.com

Are you looking for Finance?

Are you looking for Money to enlarge your business?

I think you have come to the right place.

We offer Cash at low interest rate.

Interested people should please contact us on

For immediate response to your application, Kindly

reply to this emails below only. diskanke@hotmail.com

Mr Kanke

ds.kanke@gmail.com